Published on

- 6 min read

The 50/30/20 Budget Rule: Your Simple Blueprint for Financial Freedom

Let us be real — the word “budget” sounds boring. It feels like a restriction, a punishment, something that says “no fun allowed.” But what if I told you there is a budgeting method so simple that it takes just 5 minutes to set up, and it actually works?

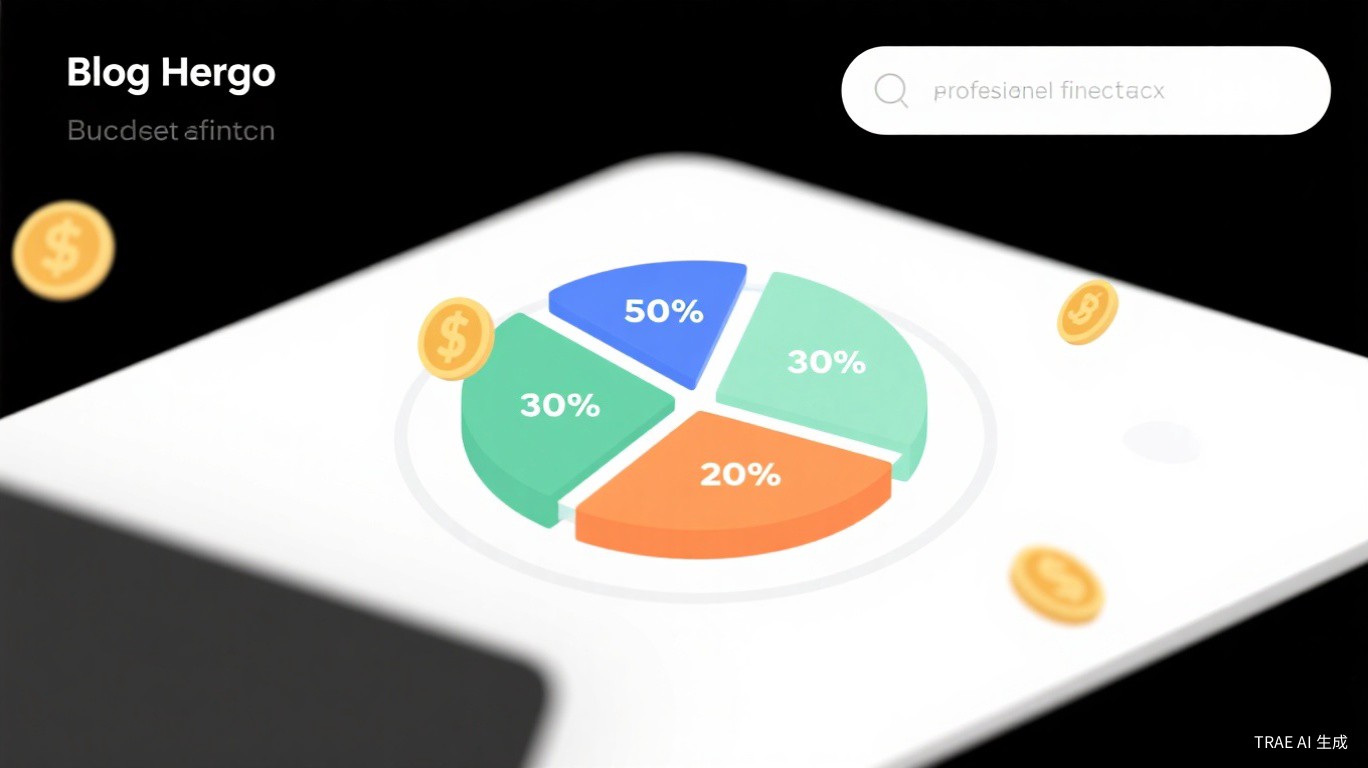

That is the 50/30/20 Rule. It is not a new app, not a complex spreadsheet, and not something that requires a finance degree. It is a simple formula that divides your after-tax income into three clear buckets:

- 50% for Needs

- 30% for Wants

- 20% for Savings and Debt Repayment

This rule was popularized by Senator Elizabeth Warren, and it has been helping millions of Americans take control of their money ever since. In this article, we will break it down so simply that you will be ready to start tonight.

What Does Each Category Actually Mean?

50% — Needs (The Non-Negotiables)

These are the expenses you literally cannot live without:

- Rent or mortgage payment

- Utilities — electricity, water, internet, and basic phone service

- Groceries — food at home, not dining out

- Car payment and mandatory insurance

- Minimum debt payments on student loans, credit cards, or other obligations

- Health insurance and essential medical costs

- Basic commute costs to maintain employment

The key word here is minimum. If your rent is eating up 60% of your income, that is a signal that something needs to change — either you need more income or you need to find a more affordable living situation.

30% — Wants (The Life Enjoyers)

This is where people often get confused. Wants are not just obvious luxury items — this category includes everything that makes life enjoyable but is not strictly necessary for survival.

- Dining out, takeout orders, and coffee shop visits

- Entertainment subscriptions (Netflix, Spotify, etc.)

- Hobbies and recreational activities

- Gym memberships (unless medically required)

- Vacations and travel

- New clothes beyond basic necessities

- Gifts for others

Here is the key insight: the 50/30/20 rule is not about deprivation. It explicitly builds in 30% of your income for enjoyment. The goal is conscious spending, not zero spending.

20% — Savings and Debt Repayment (Your Future)

This is the category that separates those who get ahead from those who stay stuck. This 20% goes toward:

- Emergency fund contributions

- Retirement savings (401(k), IRA, etc.)

- Extra debt payments beyond minimums

- Investment accounts

- Down payment savings for a home

Critical note: If you have high-interest debt (credit cards with 18%+ APR), consider flipping this priority. Put 30% toward debt repayment and 20% toward wants until you are debt-free. The math overwhelmingly favors eliminating high-interest debt first.

How to Calculate Your 50/30/20 Budget

Step 1: Determine Your After-Tax Income

Look at your paycheck. If you earn $4,000 per month after taxes, that is your starting number. If you are self-employed or have variable income, use a three-month average.

Step 2: Do the Math

Using $4,000 as an example:

- 50% for Needs: $4,000 × 0.50 = $2,000

- 30% for Wants: $4,000 × 0.30 = $1,200

- 20% for Savings: $4,000 × 0.20 = $800

That is it. Those are your monthly spending targets.

Step 3: Track and Adjust

For one month, simply track where your money actually goes. Do not judge it — just observe it. Then compare your actual spending to the 50/30/20 targets.

Real-World Examples

Example 1: Sarah, $3,500/month after taxes

- Needs ($1,750): $1,200 rent, $150 utilities, $200 groceries, $200 car/insurance

- Wants ($1,050): $300 dining out, $100 subscriptions, $200 hobbies, $450 miscellaneous

- Savings ($700): $300 emergency fund, $400 retirement

Sarah is right on track. She has breathing room in every category and is building wealth consistently.

Example 2: Mike, $5,000/month but struggling

- Needs ($3,500): $2,200 rent (luxury apartment), $300 car payment, $400 groceries, $600 other

- Wants ($1,200): Already over budget on needs

- Savings ($300): Barely saving anything

Mike’s problem is clear: his needs are consuming 70% of his income. He either needs to earn more or reduce his fixed expenses — likely by moving to a less expensive apartment or getting a cheaper car.

What If Your Numbers Do Not Match?

If Needs Exceed 50%

This is the most common problem. Solutions:

- Increase income — side hustle, negotiate a raise, find a higher-paying job

- Reduce housing costs — move to a cheaper area, get a roommate, downsize

- Lower transportation costs — sell the expensive car, use public transit, carpool

- Refinance debt — lower interest rates reduce minimum payments

If You Cannot Hit 20% Savings Yet

Start with what you can. Even 5% or 10% is better than 0%. The goal is progress, not perfection. As your income grows or expenses decrease, gradually increase your savings rate.

If You Are Debt-Free and High-Income

Consider flipping to a 50/20/30 approach — 50% needs, 20% wants, 30% savings. Or even more aggressive savings if you are pursuing financial independence.

Tools to Make This Easier

You do not need expensive software. Free options work great:

- Spreadsheet: Create three columns (Needs, Wants, Savings) and track monthly

- Mint: Automatically categorizes transactions

- YNAB (You Need A Budget): More hands-on, excellent for accountability

- EveryDollar: Simple zero-based budgeting app

- Pen and paper: Sometimes the simplest method is the most effective

The Psychology Behind Why This Works

The 50/30/20 rule succeeds because it addresses the psychological barriers that make budgeting fail:

1. It is simple enough to stick with. Three categories. No micromanaging every coffee purchase. You can hold three numbers in your head.

2. It builds in enjoyment. Thirty percent for wants means you can actually live your life while getting your finances in order. This prevents the burnout that causes people to abandon strict budgets.

3. It forces hard decisions. When your needs exceed 50%, you cannot hide from the math. You must either earn more or spend less on fixed expenses.

4. It prioritizes your future. Twenty percent minimum toward savings ensures you are always moving forward, even if slowly.

Common Mistakes to Avoid

Mistake 1: Miscategorizing Wants as Needs

Netflix is not a need. Dining out is not a need. A $800 car payment when a $400 car would work is not a need. Be honest with yourself.

Mistake 2: Ignoring the 20% Savings

It is tempting to skip savings when money feels tight. But even small amounts compound over time. Start with 5% if 20% feels impossible, but commit to increasing it regularly.

Mistake 3: Not Adjusting for Life Changes

Your 50/30/20 budget should evolve. When you get a raise, increase your savings percentage before increasing your wants. When you pay off debt, redirect those payments to savings.

Mistake 4: Perfectionism

If you hit 52/28/20 one month, that is fine. If you hit 45/35/20, that is also fine. The goal is directionally correct spending over time, not mathematical perfection every single month.

Advanced Variations

Once you master the basics, consider these adaptations:

The 60/20/20 (High Cost of Living Areas)

In cities like San Francisco or New York, 50% for needs may be unrealistic. A 60/20/20 split acknowledges reality while still prioritizing savings.

The 40/30/30 (Aggressive Savers)

If you are pursuing early retirement or have aggressive financial goals, flip wants and savings. Live on 40% needs, 30% wants, save 30%.

The 50/30/20 Plus Windfalls

Use your regular income for the 50/30/20 split, but direct 100% of bonuses, tax refunds, and gifts to savings or debt repayment.

The Bottom Line

The 50/30/20 rule is not magic. It will not solve income problems or eliminate necessary expenses. But it will give you clarity. It will force you to confront where your money actually goes. And it will provide a framework for making better decisions.

Most importantly, it proves that budgeting does not have to be miserable. You can enjoy your life today while building security for tomorrow. The 50/30/20 rule is not about restriction — it is about intentionality.

Start tonight. Calculate your numbers. Look at where you are actually spending. Make one small adjustment. That is how financial freedom begins — not with a dramatic transformation, but with a simple decision to take control.

Related Articles

Why Your Savings Account is Costing You Money

Discover why keeping all your money in a traditional savings account might be silently eroding your ...

6 Costly Money Mistakes Most Americans Make

Learn about the six most common and expensive financial mistakes that keep Americans broke, and how ...

How to Save $1,000 a Month: A Realistic Guide

A practical, step-by-step guide to saving $1,000 per month without extreme frugality or sacrificing ...